Time is Running Out (Part 1)

Warning shots have been fired, ignore at your own peril

Three years ago, I came to the conclusion that the world as we know it will cease to exist, and a new one shaped by three global orders undergoing seismic shifts will be forced upon us - slowly at first, and then, all of a sudden. That realization is why I began planning our family’s journey to navigate through the tumultuous times ahead, out of which FoFty was born.

The three global orders I am referring to are:

Financial

Geopolitical

Digital

Make no mistake, all three are interrelated with each other - they feed upon and catalyze each other. In reality, warning shots have already been fired on all three fronts as you are already aware. As these topics can get very broad and FoFty is not a financial / political / tech think tank, we are going to keep our focus on the intersection of all three in the middle, and how that translates to you as an individual and as a family.

Today in Part 1 of this series, we are going to talk about the Global Financial Order, the changes it is undergoing, and how the other two changing global orders are shaping it. In Part 2, I will discuss what these changes in the Global Financial Order mean to you and your family, and I how I took action to prepare for it.

The Existing Regime

Don’t worry, I’m not going to take you down some long-winded diatribe that rehashes all the missteps (yes, we screwed up and continue to do so) that led us here. Instead, I will simply enumerate a cycle that humanity has repeated over and over again since the Roman Empire and beyond:

1. Currency (paper money) is tied to some physical asset (gold in the current cycle - btw, did you know that before the Dollar, the US currency was the Continental? In fact, its failure is why we start with #1)

2. Too much debt is accumulated, because we are a greedy species that likes to spend money that we don’t have

3. The tie to the physical asset (gold) is severed, so that more debt - and spending - can be taken on (President Nixon in 1971, removal of US Dollar peg to gold)

4. Interest rates now control the cost of money (or the price paid to borrow money)

5. Too much debt is accumulated (did I mention we are a greedy species?)

6. Quantitative easing is invented (to “save us” after housing crash in 2007/8)

7. Too much debt is accumulated (well, what did you expect?)

8. Fiscal and monetary authorities (The Fed and US Treasury) gang up to directly stuff money into individuals’ pockets (stimmy checks)

9. Too much debt is accumulated (we just can’t help ourselves)

10. Inflation begins to appear (“transitory” inflation in 2022, we can laugh at that now)

11. Central banks have no choice but to raise interest rates (Silicon Valley Bank and friends implosion)

12. Cost to service national debt skyrockets due to higher interest rates (now higher than total annual spend on military and only second to social security/medicaire)

13. Cost to service national debt becomes too high as % of GDP (imagine interest payments on your mortgage exceeding your take home salary)

14. Central bank has no choice but to lower interest rates to stop runaway train

15. Currency debasement ensues

16. Eventually, faith in currency and debt markets wither away and a new regime is created in a “reset” -> go to step #1

So, we are about to enter step #14, with the entire world watching in anticipation of the US Federal Reserve to start cutting interest rates for the first time after raising it at the fastest pace in history to combat what they thought was “transitory inflation.”

Sure, they will say they are engineering a “soft landing” after having slayed the inflation beast. By the way, the Fed has never in its history achieved a soft landing - but somehow they will get it done right here, right now.

Source: trust me bro.

In reality, they are behind the curve of triggering a recession and backing off from bankrupting the nation from impossibly high interest rate payments.

Don’t believe me? Then take a look at this:

The Unexpected Ripper

Everything was going swell actually… even after that annoying blip of 2007-2008 when the housing crisis threatened to upheave the system. Tons of money was printed to save the Too Big To Fail banks, even more debt was taken on, and magically inflation was nowhere to be seen. I call this the Goldilocks period.

And then… the unthinkable happened: Covid.

There was a point where “is the world going to end” flashed through our minds. I know it did for me. And it must have for others, because the Fed did something even more unthinkable than Covid itself: they printed money like there was no tomorrow, and even stuffed it directly into people’s pockets!

Hello Stimmy Check!

I don’t know about you, but when I see any chart that has a vertical line going up, I cringe because I know bad things always follow parabolic vertical lines.

Somehow, the academic geniuses running the show did not think exploding this much money into existence all at once will not have consequences: I mean, more money chasing the same goods and services (or less since everything was shut down during Covid) will result in higher prices right?

Call me stupid, but that’s what I thought. And that’s exactly what happened. We finally let the inflation genie out of the bottle.

The part that frustrates me is how these geniuses kept downplaying the inflation staring at them in their faces by calling it transitory for so long. I mean, it was literally an insult to our intelligence folks - you see something but they try to talk you out of what’s literally in front of your eyes. Listen, I trust my eyes… and my brain. If I see an apple in front of me, no amount of talking by these geniuses is going to make me think it’s a tomato.

Finally, they had to admit that it was indeed an apple in front of us, and so they started raising interest rates in spectacular fashion to “catch up.” In fact, they raised interest rates so quickly that it was the fastest ever in history.

Guess what? There were unintended consequences, the first of which was the implosion of Silicon Valley Bank and friends. Remember that? Yes, that was just last year.

Well, just last week, we had another major unintended consequence, but this time, instead of some regional bank, it was the 3rd largest economy on the planet: the unwinding of the Japanese Yen carry trade. I’m not going to go into the details of what happened there, but suffice to say it was ultimately the result of a prolonged discrepancy between high US interest rates and perennially low Japanese interest rates sparked by global inflation that finally caught up to the fat cats.

Trust me when I tell you that there will be more of these unintended “financial accidents” that nobody foresaw coming, coming. Why should you believe me? Because I followed my own advise and cashed in:

The Geopolitical Financial Accelerant

Meanwhile, over in Geopolitical land and the road away from a unipolar world to a multipolar world, we have recently seen multiple wars erupt.

The Russo-Ukrainian war has further cemented the the pathway, as each side jockeys up. Ever play street ball? Two team captains, usually the strongest players, start picking teammates to battle out. The same thing is going on, within the financial context.

There is the existing regime, as highlighted above. And there is the new challenger, which is called the BRICS+. China, Russia, India, Iran and friends (note this list includes the world’s two most populous nations) have setup an alternate global banking system that can operate separately from the one the US and its allies created after winning World War II.

And it works.

How do we know? Just look at what happened to Russia after it entered the Russo-Ukrainian conflict. Despite all the sanctions - which is how the US weaponizes its dollar’s status as the world reserver currency - Russia’s economy is thriving. It has figured out how to create dark shipping pools to transport oil. It has learned, through BRICS+ which includes China, how to settle trades directly with its allies completely separately from the existing regime’s global banking system.

Not only does this challenger have legs, the legs look like they have some muscle!

The Digital Two Face

Straddling the other two global orders is the new kid on the block: the Digital World Order. And boy, this whiz kid is like the Flash!

In the context of finance, there are two areas to note.

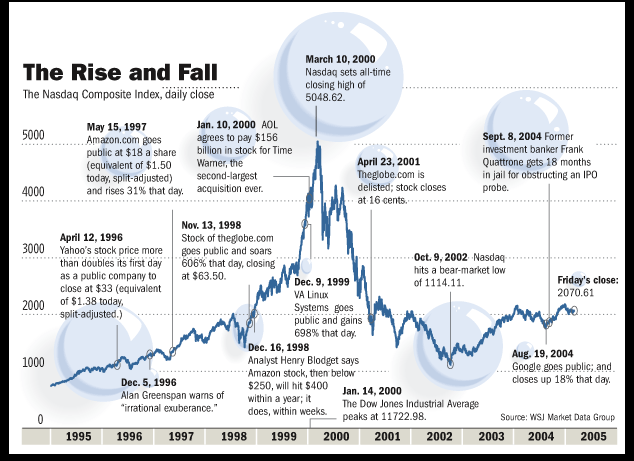

The first of which, is AI. I’m not talking about how it’s going to change our lives. I’m talking about how AI is in a stock market bubble similar to the DotCom bubble that popped in 2000 and fell over 75% (Nasdaq):

The AI bubble may have recently popped - we will need more time to confirm this, but as of this writing (Aug. 10, 2024) it is possible that we may have already seen to top of the Nasdaq for this cycle.

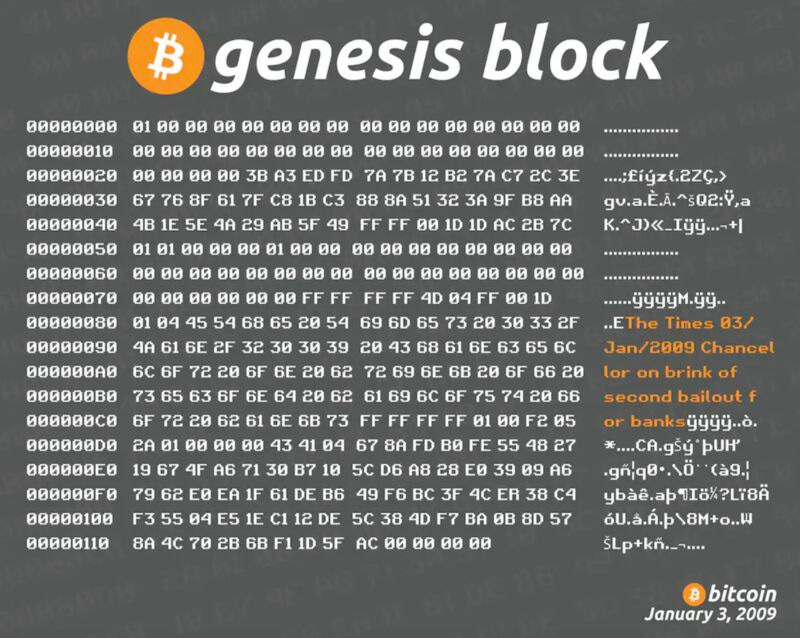

The second area of note is in the world of Bitcoin, crypto, and blockchain. Never forget, the reason Bitcoin was created was because of the 2007-2008 financial crises that led to all the money-printing by the central banks, for the banks. People, folks who we still actually don’t know to this day, got tired of the Monopoly money games the governments were playing and decided to create a new monetary paradigm that can never be centralized.

Don’t believe me? Then just have a look at bitcoin’s Genesis Block:

What’s this? Do we have another challenger? It looks like we do, but wait - there’s more!

Central banks despise alternate forms of money - and that includes Gold and Bitcoin. They realize that they cannot prevent them from manifesting though, and earlier attempts in the past to make possession of Gold Bullion illegal have failed. The same will be likely true for Bitcoin.

Therefore, the Central banks’ alternative is to join the bandwagon and build their own digital currencies - known as Central Bank Digital Currencies or CBDCs. If you think this is a new thing that they are still experimenting with, know that legislation has already been passed, and they have run trial tests many times over under the guise of “cyber attack prevention.”

Just have a look at this website to see the developmental phase of CBDCs around the world (yes, this is a global phenomenon): https://cbdctracker.org/

CBDCs are the exact opposite of Bitcoin and other cryptocurrencies even if the underlying technology may share some similar characteristics. With CBDCs, the state can monitor and control exactly how one spends money. It is in fact the ultimate tool to control spending and thus behavior. I don’t have to explain the perils of such a system of control can introduce, only because… I think I’ve mentioned how greedy humans are a couple of times already if you scroll up.

A Swirling Dance

I hope by now I’ve surfaced enough pivotal developments in the Financial World Order to make you understand that we are approaching a watershed moment. The developments are subtle at first, and slowly build momentum until suddenly, there is an eruption accompanied by the other two World Orders.

Together and in conjunction, they will usher in a new era. The challengers have emerged, and the team captains are settling their team picks.

Preparing ahead of time for this event in a non-reactionary way will yield the best results, and in the next post and video, I will discuss the tangible impacts they will have to individuals and how I’ve made changes to prepare for the coming turning.

Hi Shin, a great article . . I followed with interest. I feel the same forces at play. And have a plan B to get out of dodge to a less dense self sufficient lifestyle should there be a global hot war on top of the on-going cold war between Nato countries and China / Russia. Such an interesting time to be alive. Question, will you go over how to protect oneself in the event of the above scenario? Thanks again. . David

Fascinating read, and something similar has been simmering below the surface for me too around the same high level themes! But you expand on each in far more data and detail than I ever have and it helps validate everything more for me! Yeah agree its time for people to try and break free from the system as much as possible and look after themselves financially as the powers that be, are going to steamroll over all of us!